Financial review for current quarter and financial year to date

Current quarter (“2Q 2026”) against preceding year corresponding quarter (“2Q 2025”)

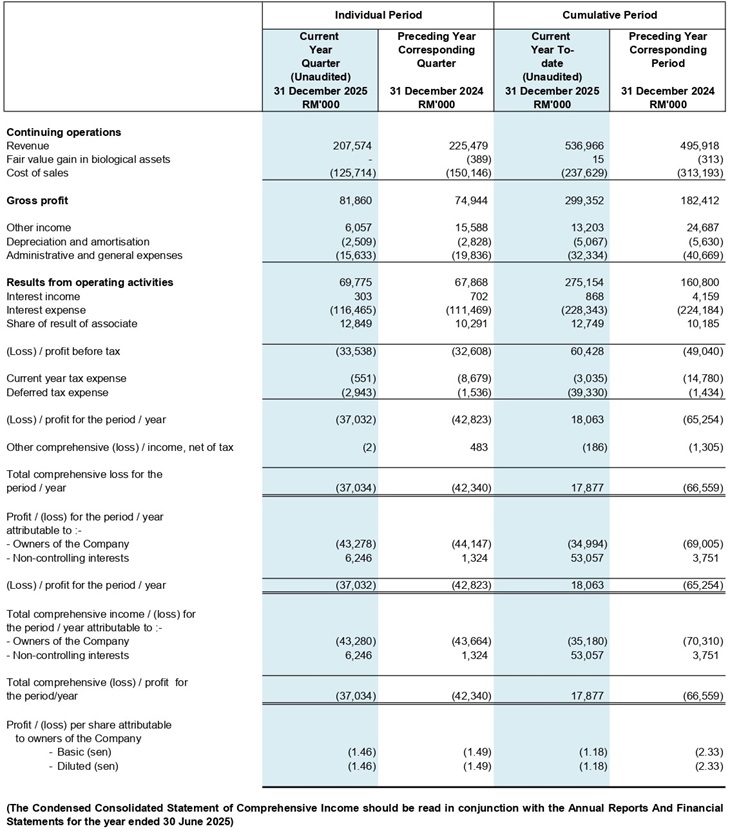

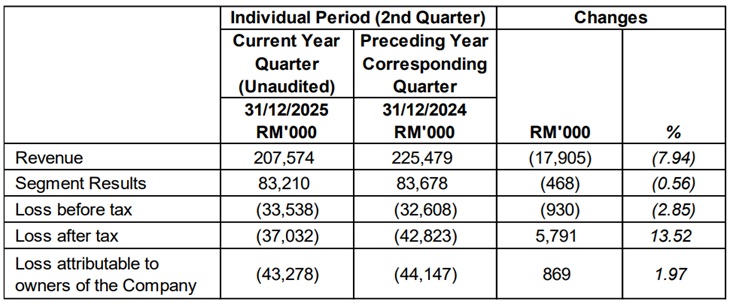

For the 2Q 2026, the Group reported a revenue of RM207.574 million and a loss before tax of RM33.538 million as compared to the revenue of RM225.479 million and a loss before tax of RM32.608 million reported in the 2Q 2025.

The performance of the respective operating business segments for the 2Q 2026 under review as compared to the 2Q 2025 is analysed as follow:

Construction operations

The construction segment recorded revenue of RM71.602 million in 2Q 2026, compared to RM100.041 million in 2Q 2025. The decline was mainly due to a lower quantum of certified progress for the RTS Link project during the current quarter, relative to the corresponding period last year. In line with the softer revenue performance, segment profit decreased to RM9.790 million in 2Q 2026 from RM16.844 million in 2Q 2025.

Property development

The property development segment reported higher revenue of RM10.227 million in 2Q 2026, compared to RM7.761 million in 2Q 2025. The increase was mainly driven by contributions from the Group’s new development, EkoTitiwangsa, which served as the primary source of revenue during the period.

Despite the higher revenue, the segment’s profit moderated slightly to RM0.171 million in 2Q 2026 from RM0.248 million in 2Q 2025. This was primarily attributable to the recent commencement of revenue recognition for EkoTitiwangsa, which is based on the stage of completion. At its current early stage of development, the recognised revenue has yet to fully absorb certain fixed and ongoing costs, including sales and marketing expenses as well as finance costs. Nevertheless, the project is progressing as planned, and profitability is expected to improve as construction advances and reaches higher stages of completion.

Toll operations

The toll operations segment reported higher revenue of RM86.045 million and a segment profit of RM68.633 million in 2Q 2026, compared to RM73.699 million in revenue and RM58.869 million in profit in 2Q 2025, representing an increase of approximately 16.75% in revenue. The stronger performance for the current quarter was mainly supported by higher toll collections across both the DUKE Highway and the SPE Highway, reflecting continued traffic growth and stable operational performance compared to the corresponding quarter of the previous year.

Plantation

For the current quarter 2Q 2026, the plantation segment registered a lower revenue of RM27.847 million and a segment result of a profit of RM9.036 million as compared with revenue of RM32.397 million and segment result of a profit of RM10.777 million in the preceding year corresponding quarter. The decrease in revenue and earnings were mainly attributed to the decline in the average selling prices for the fresh fruit bunches.

Property Investment and others

The property investment segment, comprising the EkoCheras Mall and the INNSiDE by Meliá Hotel, continued to deliver stable performance during the current quarter. The segment recorded revenue of RM11.853 million and a segment profit of RM2.032 million in 2Q 2026, broadly consistent with the RM11.581 million in revenue and RM1.788 million in profit reported in 2Q 2025. The steady performance reflects sustained occupancy rate and stable rentals contributions from the segment.

Current year to date (“YTD 2026”) against preceding year corresponding period (“YTD 2025”)

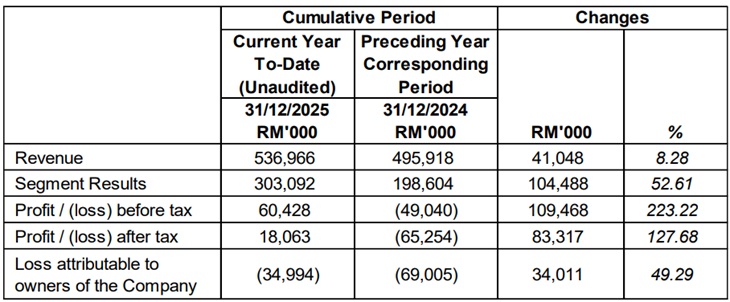

For YTD 2026, the Group reported revenue of RM536.966 million and a profit before tax of RM60.428 million, compared to revenue of RM495.918 million and a loss before tax of RM49.040 million in YTD 2025. The increase in profit before tax for YTD 2026 was primarily attributable to the toll compensation amounting to RM140.953 million received from the Government during the year, relating to the toll�'rate freeze for calendar year 2024.

The performance of the respective operating business segments for the YTD 2026 under review as compared to the YTD 2025 is analysed as follows :

Construction operations

The construction sector recorded a revenue of RM129.656 million and a segment profit of RM17.866 million for YTD 2026, compared to RM170.112 million in revenue and RM43.178 million in segment profit for YTD 2025. The decline in both revenue and segment profit was primarily due to the reduced volume of work certified for the RTS project during the year, as compared to the corresponding period in the previous year.

Property development

The property development segment for the YTD 2026 reported a lower revenue of RM17.280 million as compared to preceding year corresponding period of RM96.446 million. Similarly, the segment's result has declined from a profit of RM21.258 million in YTD 2025 to a marginal loss of RM0.013 million in YTD 2026. This variance was primarily due to the recognition in YTD 2025 of two Sale and Purchase Agreements entered into by Ekovest Properties Sdn Bhd, a subsidiary of the Company, with Airman Sdn Bhd for the disposal of sixteen (16) parcels of land, which resulted in significantly higher revenue and profit in the prior period.

Toll operations

The toll operations sector saw a significant increase in revenue, reaching RM308.210 million in YTD 2026, up from RM147.318 million in YTD 2025. Segment profit also improved substantially, increasing to RM274.660 million in YTD 2026 compared to RM121.711 million in the previous year. This strong growth was mainly driven by the recognition of toll compensation amounting to RM140.953 million during YTD 2026, relating to the toll�'rate freeze for calendar year 2024.

Plantation

The plantation sector registered revenue of RM57.519 million in YTD 2026, compared to RM58.080 million in YTD 2025. Despite the marginal decline in revenue, the segment’s results improved, with profit rising from RM18.159 million in YTD 2025 to RM20.319 million in YTD 2026. This improvement reflects better operational efficiency and stronger cost management during the current period.

Property Investment and others

The property investment and other segment’s revenue remained stable at RM24.301 million in YTD 2026, compared to RM23.962 million in YTD 2025. Segment results, however, recorded a slight decline from RM4.898 million to RM3.979 million, primarily due to some final non�'recurring exit costs incurred in connection with the closure of the Group’s F&B operations.

The Board remains optimistic about the future growth prospects of the Group’s business segments and is confident that each segment will continue to contribute positively to the Group’s performance for the current financial year ending 30 June 2026.

SPE was fully opened to the public on 3 November 2023, following a three-year delay from its original schedule due to government-directed alignment changes and pandemic-related restrictions. Notwithstanding the delay, SPE is expected to benefit from traffic inflows from the Group’s established DUKE 1 and DUKE 2 highways, as well as from its strategic integration with the surrounding highway network. The strong connectivity among these corridors is anticipated to channel additional vehicles from DUKE 1 and DUKE 2 into SPE, thereby enhancing overall traffic volumes across the network.

In addition, the Group is pursuing compensation from the Government to address losses and increased expenses incurred as a result of delays not attributable to the Group. The Board remains confident that the combined SPE–DUKE network will serve as a key long-term growth driver for the Group.

As SPE traffic continues to build and reach maturity, the tolling division’s financial performance will strengthen, enabling the Group to absorb finance costs more comfortably. The Board remains optimistic that SPE will become a significant long-term contributor to the Group’s earnings. The gradual ramp-up of SPE, supported by the maturing traffic volume, is expected to progressively mitigate the impact of the higher financing cost.

In the property development and construction segments, the Group will continue to actively pursue new opportunities aligned with its strategic objectives. Our new EkoTitiwangsa development will serve as a key driver of growth in the property segment.

On the construction front, the rationalisation of scope under the Rapid Transit System Link (“RTS Link”) project is expected to contribute positively to revenue and earnings. The Group’s construction pipeline was further strengthened following the Government’s approval on 5 May 2025 for the proposed privatisation of Phase 1 – The Laluan Istana – Kiara Expressway (LIKE) and Phase 2 – Kampung Baru Link Expressway (KBL).

Upon finalisation of the concession agreement and achieving financial close for Phase 1 – Project LIKE, the Group will promptly mobilise its resources to commence construction, reinforcing its position in the infrastructure development sector. The Group is also working concurrently with relevant government agencies to obtain necessaries approval for the potential Phase 2 – Project KBL with the objective of commencing construction work thereafter.

Separately, the Group’s subsidiary, PLS Plantations Berhad (“PLS”), is integrating its traditional cyclical oil palm business with cash crops, alongside upstream and downstream activities. The transformation also includes the durian segment, which despite its longer gestation period offers strong long-term potential. Currently, durian revenue is mainly derived from trading, while the Group continues to invest in developing its own plantations.

Upstream durian investments will remain a key focus, supporting future growth of downstream operations as the plantations mature. This transformation is aligned with the Group’s long-term strategy to diversify its revenue base and reduce reliance on the construction and property development segments, thereby promoting more sustainable and resilient growth.